The CIA is Investing Billions Into These Companies. Here's How to Copy Them - Ivan Patriki

This is how you find the next Palantir; In-Q-Tel

Ethics aside, before you think about changing the world, you need a seat at the table.

The current elite have a seat, you don’t. They are smarter are more ruthless than you.

Ask yourself: Why are they smarter? What do they know, that you don't?

While you look at Twitter, they’re studying what the CIA is betting on.

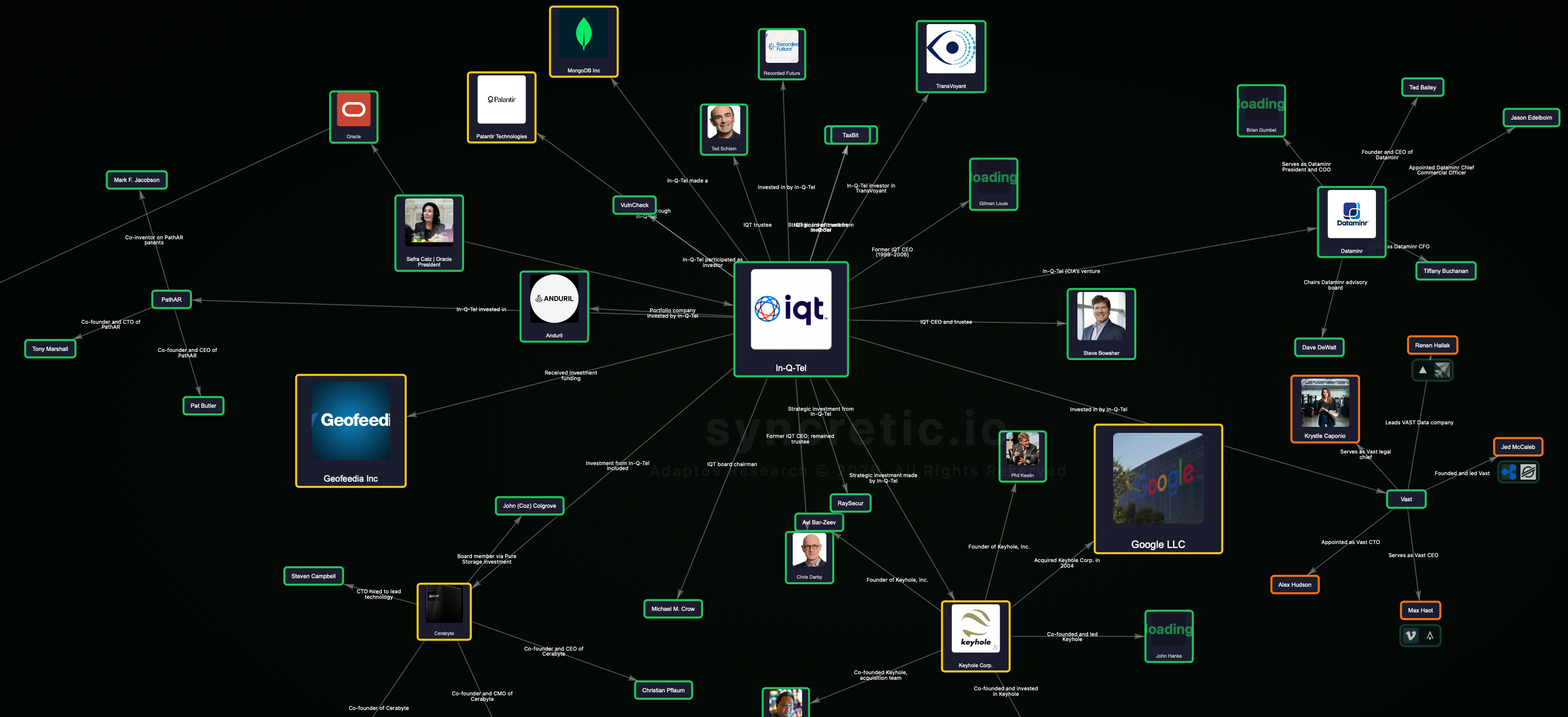

While the average investor is watching CNBC and chasing whatever stock went up yesterday, a small group of insiders has been quietly tracking the CIA’s own venture capital firm for years. They followed the money into Palantir when nobody was talking about it. They knew about Google Earth before it was Google Earth. They saw Databricks coming when data warehousing was considered the most boring sector in tech.

The information they were using has been publicly available the entire time. It lives at iqt.org/portfolio. The name of the firm is In-Q-Tel. And once you understand how it works, the pattern becomes almost embarrassingly obvious.

This is not a conspiracy theory. This is publicly documented. And if the people running the largest funds in the world are using it, you should be too.

What In-Q-Tel Actually Is

Let’s be real about what this thing is.

In-Q-Tel is the CIA’s investment arm. Full stop. It was created in 1999 by then-CIA Director George Tenet because the agency looked around and realized the most powerful surveillance and intelligence technology in the world was no longer being built inside government labs. It was being built by 25-year-olds in San Francisco who had no interest in dealing with government procurement processes.

So rather than wait 10 years for a defense contractor to build something mediocre, they created a private venture capital firm, funded it with taxpayer money, and sent it to Silicon Valley to buy stakes in the companies building exactly what the CIA needed. The name “In-Q-Tel” is literally a reference to Q from James Bond. The guy who builds the spy gadgets. That is not a coincidence. That is the whole point.

Legally it is structured as an independent nonprofit, which is how it avoids certain disclosure requirements. It receives funding through contracts with the CIA and other agencies, but is not technically “owned” by any of them. That structure is important because it means the full scope of what it invests in and what those companies do for the government is partially classified. You can see who they funded. You cannot always see what was built.

Here is what that means for you as an investor. Every company In-Q-Tel writes a check to has already cleared one of the most rigorous customer qualification processes on earth. The CIA’s analysts looked at the technology, determined it solved a real problem they have, and decided to fund it. That is not a letter of intent. That is a guaranteed revenue relationship with a customer that has a black budget and does not negotiate on price.

The company gets the money, gets the government contract, and gets the credibility that comes from being a CIA-backed vendor. Then the commercial market pays attention. Then the institutional investors follow. Then retail investors find out about it - usually right around the time the stock has already moved 300 percent.

The information about what they are investing in has always been public. The portfolio is posted on their website. Most people just never thought to look.

The Wins: What Getting It Right Looks Like

The track record is what separates this from speculation. When IQT gets it right, it does not just get it a little right.

Keyhole became Google Earth. IQT’s portfolio includes early investments in companies such as Palantir Technologies and Keyhole Inc., which Google later acquired and transformed into Google Earth, demonstrating IQT’s foresight and ability to anticipate technological revolutions with far-reaching national impact. A small satellite imagery startup, funded by the CIA to give Pentagon mapping analysts better tools. Google recognized the same technology had a billion-user application, bought it, and turned it into the most-used navigation tool in human history. IQT saw both possibilities at once.

Palantir is the most dramatic example in the portfolio. Palantir may well be the clearest sign that Silicon Valley has shacked up with the Pentagon for good. It was recently valued at $250 billion, surpassing traditional defense contracting titans like Northrup Grumman, Lockheed Martin, and General Dynamics, even though its revenue is just a fraction of those giants. Anyone who understood IQT’s backing years before the IPO had every signal they needed. The stock hit $6 at its 2022 lows. It ran to $207 before pulling back. That is a 3,000 percent move that was hiding in plain sight.

Recorded Future exited at a 3x multiple. Recorded Future received initial funding from Google and In-Q-Tel. The company specializes in the collection, processing, analysis, and dissemination of threat intelligence. It was later acquired privately by Insight Partners for $780 million, then Mastercard completed its acquisition of Recorded Future in December 2024, adding AI-driven threat intelligence capabilities to its cybersecurity services for $2.65 billion. Every step of that value creation was preceded by IQT’s early stamp.

Databricks is the sleeper. In 2016, In-Q-Tel made one of its most successful investments in Databricks, a data warehousing and AI platform that is currently valued at $43 billion, which pulled in $1.6 billion in 2024 alone. IQT invested years before AI became a cultural moment. The intelligence community was building the use case internally. Databricks is now one of the most anticipated IPOs in the market.

What ties all of these together is a simple pattern: IQT identifies a technology the government desperately needs, backs the best company solving that problem, and the government contract becomes the proof-of-concept that makes the commercial market pay attention. The institutional money follows. The stock explodes.

The Losses: What Getting It Wrong Looks Like

This is the part nobody talks about when they pitch the IQT playbook. Not everything in the portfolio is a Palantir. Some of it blew up spectacularly, and understanding why is the difference between making money and losing it.

Geofeedia was the most public disaster. The company had a genuinely clever product - a live map that pulled geotagged posts from Twitter and Instagram so law enforcement could see exactly where people were in real time during protests and large events. Geofeedia specializes in collecting geotagged social media messages to monitor breaking news events in real time. The company counted dozens of local law enforcement agencies as clients and marketed its ability to track activist protests on behalf of both corporate interests and police departments.

It worked. Departments in Oakland, Chicago, Detroit, and dozens of other cities were paying for it. Then the ACLU got involved. After the ACLU’s report, Twitter said it was immediately suspending Geofeedia’s commercial access to its data. Facebook, which also owns Instagram, said it cut off Geofeedia from access to its developer platform after learning the firm violated terms of service. Following these suspensions, Geofeedia scaled back its business, cutting its sales force by half. The company never recovered meaningfully.

The lesson is brutal and simple: if your entire business model sits on top of someone else’s API, you do not have a business. You have a license that can be revoked overnight.

PATHAR followed the same trajectory. PATHAR’s product, Dunami, was used by the FBI to mine Twitter, Facebook, Instagram, and other social media to determine networks of association, centers of influence, and potential signs of radicalization. When Geofeedia collapsed under public scrutiny, PATHAR lost platform access and quietly disappeared. No IPO. No acquisition. No exit.

The pattern in both failures is identical: narrow use case, built entirely on third-party data the company did not own, with no proprietary layer that could survive losing the API access. The moment the social platforms decided the political risk outweighed the revenue, these companies ceased to exist.

Compare that to Dataminr, which survived where Geofeedia failed. Dataminr built proprietary AI on top of the data rather than simply reselling the access. When Twitter cut off Geofeedia, Dataminr eventually negotiated a different relationship because it had become genuinely valuable as an analytical layer, not just a data pass-through. That distinction is everything.

The Pattern: What Separates a Win From a Loss

After looking at the full run of IQT investments, the winners and losers split cleanly on a few factors.

The winners build proprietary technology that cannot be replicated by revoking an API key. Palantir owns the data integration architecture. Databricks owns the processing engine. Recorded Future owns the analytical model. MongoDB owns the database layer itself. None of these companies disappear if one platform changes its terms of service.

The losers build distribution on top of someone else’s infrastructure. Geofeedia was a front-end for Twitter and Instagram data. PATHAR was a front-end for the same. When the pipes got cut, there was nothing underneath. No moat. No leverage. No survivability.

The winners also have explicit dual-use applications. Government builds the initial market, commercial scales it. Keyhole’s satellite imagery was useful to the Pentagon and to every person who needed driving directions. Palantir’s data analytics were useful to the NSA and to every hospital system trying to reduce fraud. Databricks was useful to intelligence analysts and to every Fortune 500 company drowning in unstructured data.

The losers were single-use tools. Tracking protesters is not a commercial use case anyone will publicly buy. That ceiling was always going to be the problem.

The Current Watch List: Where to Position Now

The Current Watch List: Where to Position Now

Do your homework.

The IQT portfolio today reflects the same structural logic that produced the earlier winners. Government use case first, commercial explosion second. Whether the current batch follows that same trajectory is not guaranteed. Nothing in investing is. But the signals are there if you know where to look.

Below are some examples of what seem interesting, NOT FINANCIAL ADVICE.

Dataminr hired a CFO specifically to lead IPO preparations in July 2025 and raised $85 million the same year. Companies do not do both of those things in the same calendar year by accident. Whether the offering actually happens in 2026 or gets pushed is genuinely unknown. What is worth researching is why Dataminr survived where Geofeedia collapsed. The short answer is that Dataminr built its own analytical layer on top of social data rather than simply reselling API access. Whether that proprietary layer is defensible enough to support a public company valuation is a question only your own diligence can answer. Pre-IPO shares are available on secondary markets through platforms like Hiive and Forge for accredited investors, currently at a significant discount to the 2021 peak.

Anduril is easier to understand as a thesis, harder to act on. Real revenue. Real government contracts. A product suite the U.S. military has already integrated into active operations. Last private valuation was $14 billion. No IPO date announced. The defense spending environment right now historically precedes major defense IPOs, but whether Anduril times its offering to that window or waits years longer is speculation. What you have to decide is whether $14 billion is a fair entry point given the competitive landscape and what a budget shift does to that number. Reasonable people disagree.

The bioengineering plays are the most speculative category on this list by a wide margin and should be treated accordingly. IQT is funding companies combining AI with programmable biology. The potential commercial applications in drug discovery, agriculture, and industrial processes are theoretically enormous. The timeline to get there is genuinely unknown. This is not a 2026 story. It might not be a 2030 story. What is worth doing is tracking the companies now so that when the co-investor signals start appearing, you have the context to move quickly.

The IQT portfolio gives you a head start, not a guarantee. The work of turning that head start into an actual investment decision is still yours to do. Look at the portfolio. Read about the companies. Make up your own mind.

That is the only version of this playbook that works long term.

How to Read the Portfolio Like an Analyst

Most people look at the IQT portfolio and see a list of company names. Analysts look at the same list and see a map of what the U.S. government is about to spend money on for the next decade.

The difference is in knowing what questions to ask.

The first thing to look at is clustering. When IQT starts investing in multiple companies solving adjacent problems in the same time window, that is not coincidence. That is a procurement signal. In the mid-2010s they backed Databricks, Palantir, and several other data analytics companies within a few years of each other. That cluster told you the intelligence community had a massive unsolved problem around unstructured data and was throwing money at every company that looked like it could help. The correct response was to buy every publicly accessible piece of that thesis and wait. Right now the clustering is happening in AI inference hardware, autonomous weapons systems, and programmable biology. Those clusters are telling you the same thing the data analytics cluster told you ten years ago.

The second thing to look at is the founder background. IQT is disciplined about who it backs. When you see a company in the portfolio led by a former NSA director, a former DARPA program manager, or someone who spent a decade inside one of the major defense primes, that is a company that already knows how to sell to the government. They speak the language. They know the procurement process. They have the clearances. The technical risk might still be real but the go-to-market risk is essentially zero. Government sales cycles that kill normal startups do not kill companies run by people who spent their careers inside those systems.

The third thing to look at is what is missing. IQT does not invest in everything, and the gaps in the portfolio are as informative as the investments themselves. When a category of technology is obviously relevant to national security and IQT has not backed anything in it, there are two explanations. Either they have classified investments in that space that are not showing up on the public portfolio, or they looked at the category and decided no company was ready yet. Either way, that tells you something. It tells you either the technology is further along than the public narrative suggests, or there is a gap in the market that someone is about to fill and IQT will fund them when they do.

The fourth thing to look at is geography. IQT’s recent expansion into London, Sydney, Singapore, and Munich is not about international diversification for its own sake. It reflects where the allied intelligence community sees emerging threats and where the companies solving those problems are being built. When IQT opens an office in a new city, the portfolio companies coming out of that region in the following two years tend to be specifically relevant to whatever that country’s intelligence services are prioritizing. Australia’s office reflects Indo-Pacific surveillance technology. The Singapore office reflects ASEAN threat monitoring and maritime intelligence. Follow the offices to find the regional investment thesis.

The Co-Investor Signal

One of the most powerful tools in this entire playbook costs you nothing and requires no special access. It is simply watching who gets into a deal after IQT does.

Here is how the sequence typically works. IQT makes an early investment, usually at Series A or B, and the company begins developing its technology with a government contract providing baseline revenue. At this stage the company is nearly invisible to the broader venture community. It is not showing up in TechCrunch. It is not being discussed on investing podcasts. The only people who know about it are the founders, the government counterparts they are working with, and the small network of defense-focused investors who track IQT’s moves.

Then the technology matures enough to demonstrate commercial potential beyond the government use case. The company raises a larger round, and this is where the co-investor signal becomes powerful. If the Series C or D includes Andreessen Horowitz, Sequoia, General Catalyst, or any of the major multi-stage funds that have the resources to do serious diligence, that is the confirmation that the commercial thesis is real. Those funds did not invest because of the government contract. They invested because their analysts looked at the total addressable market and decided the technology had a generational commercial opportunity.

Pay attention to opportunities like this

The reason the co-investor signal matters so much is that it compresses the information asymmetry. You do not need to have read the classified government contract to know the technology works. You do not need to have sat in the product demos. You do not need to have done primary research with government buyers. Andreessen Horowitz has a $35 billion fund and a team of 200 people who did all of that work. When they write a check, they are telling you everything they found out. You just have to be paying attention.

The opposite signal is equally useful. When an IQT company raises follow-on rounds but the co-investors are smaller funds, family offices, and strategic corporate investors rather than the major growth-stage VCs, that is a sign the commercial case has not fully materialized. The technology might be working perfectly for the government use case while still failing to translate into a commercial product civilians would pay for. That is the profile of a company that ends up as a government contractor forever, never goes public at a consumer-scale valuation, and delivers modest returns to early investors instead of the generational ones you are looking for.

The distinction between Palantir and Geofeedia maps almost perfectly onto this framework. Palantir attracted serious institutional capital that believed in the commercial thesis. Geofeedia never did. By the time the ACLU report dropped and the platforms revoked access, there were no major institutional holders to ride it out. There was no commercial runway to pivot into. There was nothing underneath the government contracts except the contracts themselves.

Sector Breakdown: What IQT Is Betting On Right Now

The current IQT portfolio is not the same portfolio it was in 2015. The sectors it is most aggressively funding right now reflect where the intelligence community sees the next decade of threats and capabilities. Understanding these bets is how you get ahead of the next cluster.

AI inference and edge computing. The intelligence community’s problem is not building AI models. It is running them at the edge, in denied environments, on hardware that does not have a reliable connection to a data center. Think submarines, forward operating bases, and satellite systems that need to make autonomous decisions without phoning home first. IQT is funding companies building specialized chips and software stacks that can run large AI models locally on constrained hardware. The commercial analog of this technology is every device manufacturer in the world trying to run AI locally on phones, laptops, and cars without burning through battery life. The defense use case proves the technology under the most demanding conditions possible. The commercial market is orders of magnitude larger.

Quantum computing and post-quantum cryptography. IQT has 25 unicorns in its portfolio, including companies in the quantum computing space. D-Wave listed on the NYSE and acquired Quantum Circuits in early 2026. Tracxn But the quantum bet is not just about quantum computers. It is equally about the companies building encryption systems that can survive a world where quantum computers exist and can break current RSA encryption. Every bank, every hospital, every government system on earth will need to upgrade its cryptography when quantum computers reach sufficient scale. IQT is funding the companies that will perform that upgrade. The government is the first customer. Every financial institution on the planet is the commercial market.

Synthetic biology and programmable life. This is the newest and most ambitious cluster in the current portfolio. IQT has been building a position in companies that combine AI with biological systems, essentially applying software logic to living cells. The defense applications include biodefense, biosurveillance, and performance enhancement. The commercial applications include drug discovery, agricultural biotechnology, and industrial fermentation. This is a 10 to 15 year thesis, not a 2 to 3 year trade. But the companies being funded right now are the ones that will be acquired for billions or go public at generational valuations when the technology matures. Getting in early means getting in before the narrative exists, which is exactly when the best prices are available.

Autonomous systems and robotics. Anduril is the flagship but it is not the only company in this bucket. IQT has been systematically building exposure to the full stack of autonomous defense systems: the sensors that detect threats, the AI that identifies and classifies them, the communications infrastructure that coordinates responses, and the physical platforms that carry out actions. The commercial analog is every logistics, agriculture, and infrastructure company trying to automate dangerous or expensive physical work. The military is building the supply chain and proving out the reliability at a scale no commercial customer could afford to fund. The civilian market inherits the technology at a fraction of the development cost.

Deepfake detection and information integrity. Notable recent investments include GetReal Security, a California-based firm developing anti-AI screening systems that help detect deepfakes and other deceptive methods. Washington TimesThe intelligence community’s problem with deepfakes is obvious. The commercial problem is equally enormous. Every media company, every financial institution doing remote identity verification, every social platform trying to maintain trust is going to need this technology. IQT’s investment signals that the government has already decided this problem is critical and that GetReal’s approach is the most promising solution it has seen. Watch for the co-investors that follow.

Position Sizing and Risk Management

None of this works if you size the positions wrong.

The IQT playbook is a high-conviction, long-horizon strategy. It does not mean putting half your portfolio into Palantir or betting your savings on a pre-IPO investment in a company that might not go public for five years. It means building a diversified set of positions across the confirmed winners, the near-term IPO candidates, and the early-stage private companies, sized according to where each sits in the risk spectrum.

For public companies with established IQT provenance, like Palantir and D-Wave, reasonable position sizes are what you would allocate to any high-conviction growth stock. Meaningful enough to matter to your returns, small enough that a 30 percent drawdown does not change your life. These companies have real revenue, real government contracts, and real commercial businesses. They are not going to zero. The risk is valuation, not existential survival.

For pre-IPO private companies on secondary markets, the position size should reflect the reality that these are illiquid, speculative, and could take years to reach a liquidity event. Accredited investors who participate in secondary markets typically allocate between two and ten percent of their investable assets to the entire private markets category, not to a single company. Within that allocation, spreading across three or four IQT-adjacent private companies is more sensible than concentrating in one. Dataminr, Anduril, and a bioengineering name gives you exposure across the near-term IPO thesis, the defense hardware thesis, and the decade-long science thesis simultaneously.

For the earliest stage companies that just appeared in the IQT portfolio, the position is information, not capital. You cannot buy equity in most of these companies yet. What you can do is track them, understand the technology, map the commercial use cases, and be ready to act quickly when they either raise a public round, appear on a secondary market, or get acquired by a public company whose stock you can buy. The preparation is the position.

The single biggest mistake retail investors make with this kind of thesis is acting too late and sizing too large at the same time. They hear about Palantir at $150 and put in more than they should because they feel like they missed the early move and are trying to make up for it with size. That is the exact opposite of the right behavior. The right behavior is smaller size at higher certainty, which in this framework means the public companies, combined with earlier positioning in the private companies where the real upside still exists.

Why the Government Never Stops Writing Checks

There is a foundational question underneath all of this that is worth addressing directly: what if government spending gets cut and the whole thesis collapses?

It is a legitimate question and it deserves a real answer.

The intelligence and defense budget does not behave like discretionary consumer spending. It does not contract when inflation rises. It does not shrink when the stock market falls. It is not subject to the same political pressures that cut social programs or infrastructure investment, because the stated justification for every dollar in it is national security, and no elected official in any party has ever successfully run on a platform of making the country less secure.

The budget has grown in every decade since the Cold War. The events that accelerated the most recent growth cycles include 9/11, the rise of Chinese technological competition, the war in Ukraine, and the emergence of AI as a potential military force multiplier. None of those factors are going away. In fact, the AI element is still in its earliest stages of military adoption, which means the companies building AI-enabled defense and intelligence tools are at the beginning of a multi-decade procurement cycle, not the end of one.

There is also a structural point that gets overlooked. IQT does not just create companies that sell to the government. It creates companies that the government becomes dependent on. Once the NSA runs its data fusion architecture on Palantir, switching to a different system requires rebuilding years of institutional knowledge, retraining thousands of analysts, and accepting a period of reduced capability while the transition happens. That switching cost is one of the most powerful moats in enterprise software, and it is even more powerful when the customer is a government agency that treats continuity as a security requirement. The recurring revenue these companies generate does not come from quarterly sales cycles. It comes from multi-year contracts with renewal clauses and expansion options that compound over time.

That is the machine. It was built by the government. It runs on taxpayer money. And the returns it generates flow to the people who understood what it was early enough to position.

The list is public. The pattern is documented. The next ten years are going to look a lot like the last ten years, except the technologies will be more powerful, the commercial markets will be larger, and the companies being funded right now will be the ones everyone is talking about in 2035.

You are reading about them today.

This is not financial advice. Pre-IPO investments are speculative and only available to accredited investors. All stock investments carry risk. The information above is for educational purposes only. Do your own research before making any investment decisions.